Construction Loan vs Standard Home Loan: How Progress Payments Actually Work in Australia

A couple in Western Sydney signs a fixed-price building contract for $650,000. The numbers look manageable at the start. Their loan is approved, the land is secured, and construction is expected to wrap up within the year. A few months in, the experience starts to feel different from what they had planned.

The build doesn’t move as quickly as expected. Each stage takes time to complete, and progress depends on inspections, approvals, and contractor availability. Recent construction data shows ongoing shifts in activity levels and project timing across Australia, with builds taking longer to move from start to completion than they did a few years ago.

At the same time, their loan doesn’t behave the way they thought it would. Repayments don’t start at a fixed level. Instead, they change as the build progresses. One month the amount is lower, the next it increases slightly, depending on how much of the loan has been used. Nothing is technically wrong with the loan. It’s just structured differently.

In Australia, residential construction follows a staged process, where financing, approvals, and building progress are closely linked from early planning through to completion. That structure is what sits behind most of the confusion. Many borrowers approach a construction loan expecting it to behave like a standard home loan.

It doesn’t. And that difference becomes clearer once you look at how funds are actually released, and why the timing of those payments matters just as much as the loan itself.

The Real Difference Is in How the Money Moves

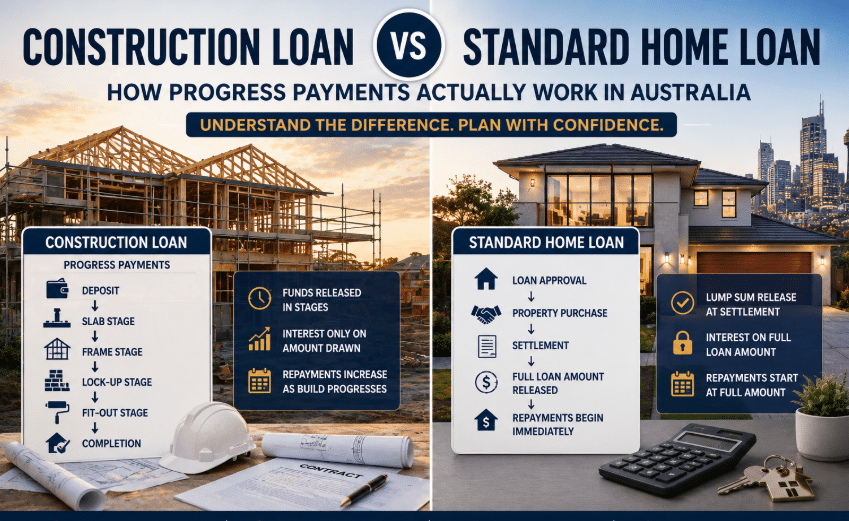

A standard home loan is built around a completed property. The bank approves the loan, releases the full amount at settlement, and repayments begin on the entire balance. A construction loan vs home loan comparison shows a different structure entirely. With a construction loan, the bank does not release the full amount up front. Funds are drawn down in stages as the build progresses.

This is not just a technical detail. It affects interest, timing, and how your cash flow behaves over the life of the build.

Standard Home Loans Follow a Fixed Path

When you’re buying an established property, the lender is dealing with something that already exists and can be valued in full from the start. That changes how the loan is set up.

Because the asset is complete, there’s no need to release funds in parts or track progress against construction milestones. The bank can approve the loan against a known value, and the entire amount is prepared for settlement. That’s why the process tends to follow a single, continuous sequence:

Standard Home Loan Stages |

| Loan Approval The lender assesses your borrowing capacity and approves the loan ↓ |

| Property Purchase You exchange contracts on an existing home ↓ |

| Settlement Legal ownership transfers to you ↓ |

| Full Loan Amount Released The full loan amount is paid to the seller ↓ |

| Repayments Begin Immediately You start repayments on the entire loan balance |

There are fewer moving parts because the asset is already complete. The lender can assess its value upfront, and the borrower knows exactly what they are paying for from day one. If you look at how home loans are typically structured, the process is linear and predictable.

Construction Loans Are Built Around Stages

A building loan in Australia works differently because the property does not yet exist in its final form. Instead of a single transaction, the loan is tied to the progress of construction. Funds are released in stages, aligned with key milestones in the build. While exact terms vary by lender and builder, most projects follow a similar sequence:

Typical Construction Loan Stages |

| Deposit Initial payment made to the builder ↓ |

| Slab Stage Foundation work is completed ↓ |

| Frame Stage Structural framing is put in place ↓ |

| Lock-up Stage External walls, doors, and windows are installed ↓ |

| Fit-out Stage Internal fixtures and finishes are completed ↓ |

| Completion Final inspection is done, and the build is signed off |

These are often referred to as construction loan stages, and each stage triggers a partial release of funds. Rather than receiving the full loan amount at once, the borrower draws down only what is needed at each point as progress payments.

Progress Payments Change How Interest Works

This is where most of the confusion sits. With a progress payments construction loan, interest is only charged on the portion of the loan that has been drawn down, not the full approved amount. That means:

- Early in the build, repayments are relatively low

- As more funds are released, repayments gradually increase

- By completion, repayments resemble a standard home loan

From a cash flow perspective, this can feel manageable at the start, but it requires planning. The increase is gradual, not optional. There is also a structural reason why progress payments exist. In Australia, construction work is tied to payment frameworks that allow contractors to claim payments as work is completed.

This ensures that builders are paid for completed work, and lenders align their funding to that same structure.

Where the Differences Actually Show Up During the Loan

Up to this point, the structure of each loan is clear. What matters more in practice is how those structures affect the borrower over time.

This is where the comparison becomes more useful. Instead of looking at how each loan is set up, it helps to look at where the differences show up during the process, particularly in how funds are released, how interest builds, and how repayments change as the loan progresses.

Comparison Based on Borrower Impact | ||

Borrower Impact Area | Standard Home Loan | Construction Loan |

| Fund release timing | Lump sum at settlement | Released in stages |

| Interest calculation | Charged on the full loan amount | Charged only on the drawn amount |

| Repayment pattern | Starts at full amount | Increases gradually over time |

| Property condition | Fully completed at purchase | Built progressively |

A construction loan vs home loan comparison becomes clearer when viewed this way. The difference is not just what you borrow, but how the borrowing unfolds over time.

Where Construction Loans Get Complicated

The staged structure introduces variables that do not exist in a standard loan.

- Construction delays can push timelines and affect repayments

- Cost variations may require additional funds or adjustments

- Valuation shifts can influence how much the bank is willing to release

- Builder coordination becomes critical to timing payments

In cases like an owner builder loan, the complexity increases further because the borrower is responsible for managing the build rather than working with a registered builder. These moving parts are not unusual, but they do require closer oversight. The system is predictable, but only if each stage aligns as expected. Legislation also underpins how payments are handled and disputes are resolved in construction projects.

Why This Matters More in Greater Sydney

In higher-cost markets like Greater Sydney, the structure of a construction loan becomes more significant.

- Build costs are higher

- Budget margins are tighter

- Delays carry a greater financial impact

When the cost base increases, even small changes in timing or pricing can have noticeable effects. A staged loan structure means those effects show up progressively rather than all at once. That can be helpful, but it also means there is less room for misalignment between the build schedule and the loan.

Where Borrowers Often Misjudge the Process

A common assumption is that once the loan is approved, the rest is handled automatically. In practice, that is rarely the case. Borrowers often underestimate:

- How repayments scale over time

- The impact of delays on cash flow

- The importance of aligning the loan with the build contract

- The need to compare loan structures, not just interest rates

Looking at different loan options early can make a noticeable difference in how the process plays out and how loan structures and rates vary.

Structuring the Loan From the Start

A construction loan works best when it is aligned properly from the beginning. That includes:

- Matching the lender to the type of build

- Structuring a land and construction loan where needed

- Ensuring drawdown stages align with the building contract

- Allowing for buffers in case of cost changes

This is where the role of a broker becomes more practical than theoretical. It is not just about finding a lender, but about ensuring the structure holds up across the entire build.

Working with a credible financial broker in Australia who understands construction loan structuring can help reduce friction during later stages. For borrowers building in Sydney, comparing loan types and lender approaches can also provide useful context. If the build is tied to first-home ownership, there may also be opportunities to align with available grants and incentives.

What This Means When You’re Choosing Between the Two

A standard home loan gives you certainty from the start. You know the property, the full loan amount is released at once, and your repayments stay consistent.

A construction loan works differently because the property doesn’t exist yet. The loan follows the build, not the other way around. Funds are released in stages, repayments shift over time, and the outcome depends on how well the structure holds together across those stages.

That’s why the decision isn’t just about interest rates or loan types. It comes down to how comfortable you are managing a loan that changes as the build progresses. If the structure is understood early, the process is manageable. If it isn’t, small gaps in timing or planning tend to show up later, usually when costs or repayments start to move.

In that sense, the difference between the two isn’t complexity. It’s how much of the process is fixed upfront, and how much unfolds as you go, which is often where guidance from a financial broker like Efficient Capital Solutions becomes useful.