Lenders Mortgage Insurance (LMI): What It Is, How Much It Costs & How to Avoid It

If you’ve been exploring the property market in Sydney, you’ve likely run into a familiar situation. You can manage the repayments, your income is stable, but the deposit feels like the final hurdle. Somewhere in that process, Lenders Mortgage Insurance comes up, and often, it raises more questions than answers.

For many borrowers, especially first-home buyers, an LMI home loan is not always clearly explained. It’s often presented as a cost you simply “have to pay.” In reality, it’s more nuanced than that. This guide breaks down how Lenders Mortgage Insurance works in Australia, what it actually costs, and, more importantly, how you can approach it strategically rather than reactively.

What Is Lenders Mortgage Insurance (LMI) in a Home Loan?

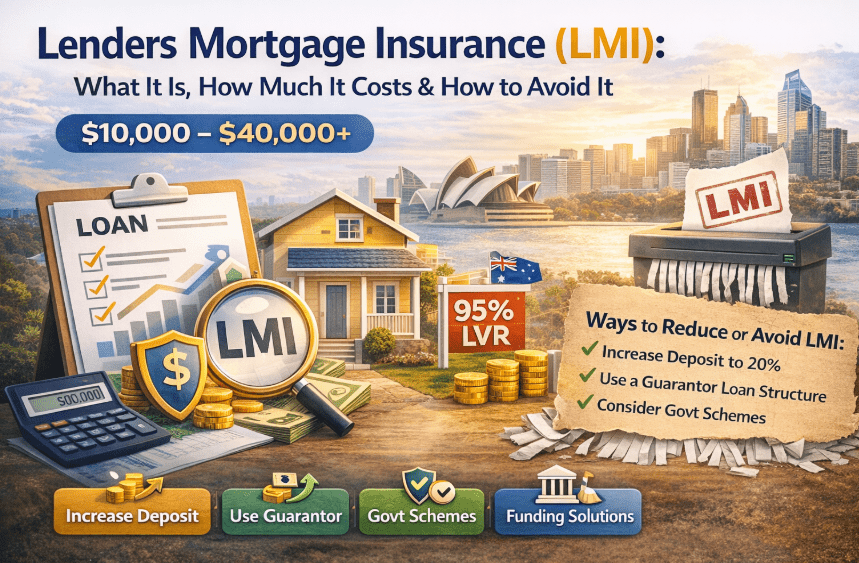

At its core, Lenders Mortgage Insurance Australia refers to a one-off fee charged when a borrower takes out a home loan with a smaller deposit. This deposit is typically less than 20% of the property value. It’s tied to something called the Loan-to-Value Ratio (LVR):

- 80% LVR → 20% deposit → No LMI

- Above 80% LVR → LMI applies

The important distinction is this: LMI protects the lender, not the borrower. If the loan defaults, the insurance covers the lender’s risk. The borrower still remains responsible for the full loan. In practice, Australian lending standards commonly align with this threshold, where loans exceeding an 80% LVR begin to attract mortgage insurance.

When Do You Actually Pay LMI in Australia?

While the 20% deposit rule is widely known, the situations where the lenders mortgage insurance applies in Australia go beyond just first-home purchases. You may encounter LMI if:

- Your deposit is below 20%

- You’re refinancing at a higher LVR

- You’re purchasing an investment property with lower equity

In markets like Greater Sydney, where property prices are significantly higher, many borrowers naturally fall into these higher LVR brackets. It’s also worth noting that buyers are not excluded from entering the market with smaller deposits. In fact, loans can be approved with deposits as low as 5%, though this typically comes with LMI due to the increased lending risk.

How Much Does LMI Cost?

One of the most common questions is around cost, and this is where things become less straightforward. There isn’t a fixed number. Instead, LMI is calculated based on several variables:

- Property value

- Loan amount

- Deposit size

- LVR

- Borrower profile

For most borrowers, LMI can range anywhere between $10,000 to $40,000 or more. If you’re trying to estimate this, many lenders internally rely on models similar to an LMI cost calculator, adjusting premiums based on risk levels and loan size.

Example: LMI Cost in a Sydney Scenario

Let’s take a simple scenario:

- Property value: $900,000

- Deposit: 10% ($90,000)

- Loan: $810,000

In this case, LMI could fall somewhere between $18,000 to $30,000, depending on the lender and borrower profile. The key takeaway is not the exact number, but how sensitive LMI is to small changes in deposit and structure.

Capitalising LMI: What It Means Long-Term

Many borrowers don’t pay LMI upfront. Instead, it’s added to the loan amount. This is called capitalising LMI. While it reduces immediate cash pressure, it increases:

- Total loan size

- Interest paid over time

For example, adding a $25,000 LMI premium to your loan means you’re also paying interest on that amount over the life of the loan.

Is LMI Always a Bad Thing?

It’s easy to assume that Lenders Mortgage Insurance is something to avoid at all costs. But that’s not always the most practical perspective. In a rising market like Sydney, waiting to save a full 20% deposit could mean:

- Higher future property prices

- Delayed entry into the market

In that context, LMI can act as a trade-off: Pay a premium now and enter the market earlier. For some borrowers, this works in their favour. For others, it may not. The difference lies in how the decision is structured.

How to Avoid LMI in Australia (Strategically, Not Just Ideally)

When people search for how to avoid LMI in Australia, the common advice is simple: “save a bigger deposit.” While that’s valid, it’s not always realistic, especially in high-value markets. Avoiding LMI is often less about saving and more about structuring smarter.

Increase Deposit to 20%

This remains the most straightforward approach. In general, borrowers who reach a 20% deposit (80% LVR) are not required to pay LMI or may use alternatives like a guarantor structure.

Use a Guarantor Loan Structure

A guarantor, who is usually a family member, can provide additional security against the loan. This effectively reduces your LVR without requiring a larger cash deposit, helping you avoid LMI.

Consider Loan Structuring Options

This is where the conversation shifts from general advice to strategy. Different loan structures can influence:

- LVR calculation

- Risk assessment

- LMI applicability

Options may include:

- Splitting loans

- Using existing assets as security

- Timing the loan differently

What often gets overlooked is that structuring decisions made early can shape the long-term sustainability of the loan. Setting the correct debt structure should be the first step in the financing process and will make sure that investments are sustainable.

LMI Waivers: Who Qualifies in Australia?

There are situations where LMI may not apply, even with a lower deposit. Certain professions are eligible for the LMI waiver policies in Australia, including:

- Medical professionals

- Lawyers

- Accountants

- Some engineers

These waivers depend on income thresholds and specific lender policies. Many eligible borrowers simply aren’t aware that these options exist.

Government Schemes That Can Help Reduce or Eliminate LMI

For first-home buyers, government-backed schemes can change the equation significantly. Under certain programs, buyers can enter the market with as little as a 5% deposit, with the government effectively supporting the loan structure. Recent updates to these schemes have also removed income caps and waitlists in some cases, while allowing eligible buyers to proceed without LMI.

Reducing LMI (If You Can’t Avoid It Completely)

In many cases, avoiding LMI entirely may not be practical. However, reducing it is often achievable. Small adjustments can make a noticeable difference:

- Increasing deposit slightly (e.g., from 10% to 12%)

- Choosing a lender with different risk pricing

- Structuring the loan differently

Even minor improvements in LVR can significantly lower the premium.

Why Loan Structure Matters More Than Just the Deposit

Two borrowers with the same deposit can end up paying very different LMI amounts. You may wonder why? Because lenders assess risk differently. Factors include:

- Income stability

- Employment type

- Asset position

- Overall loan structure

This is why Lenders Mortgage Insurance in Australia is not a fixed cost; it’s influenced by how the loan is presented and structured.

How Financial Advisory Can Help You Navigate LMI Better

At this stage, the conversation moves beyond definitions and into decisions. Understanding Lenders Mortgage Insurance is one part. Structuring around it is another. A structured financial approach can help:

- Evaluate whether paying LMI makes sense

- Identify ways to reduce or avoid it

- Align borrowing with long-term financial goals

In more complex or high-LVR scenarios, alternative funding pathways may also come into play, particularly where flexibility is required. Access to private capital markets can assist in meeting an immediate need for finance, high LVRs or complex scenarios.

Making a More Informed Borrowing Decision

Lenders Mortgage Insurance is a common part of the Australian property landscape, but it isn’t one-size-fits-all. The cost varies, the impact differs, and the outcome depends on how it’s approached.

For some, it’s a necessary step toward entering the market sooner. For others, it’s a cost that can be reduced or avoided with the right structure. What matters is not just whether you pay LMI, but whether you’ve made that decision with clarity.

For borrowers looking to approach this strategically, Efficient Capital Solutions can help structure your loan in a way that aligns with both your immediate purchase and long-term financial position.