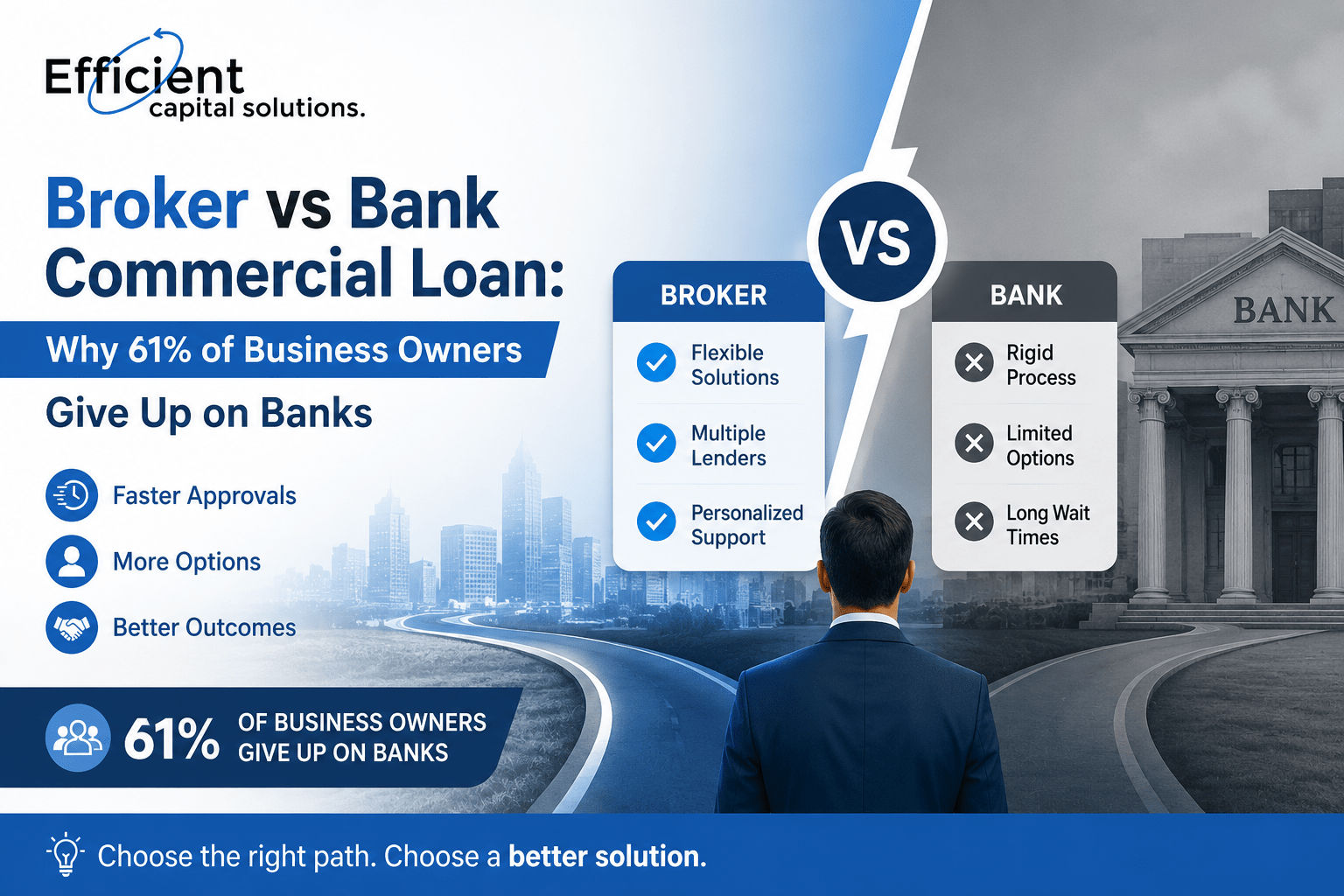

Broker vs Bank Commercial Loan: Why 61% of Business Owners Give Up on Banks

The Moment Most Business Owners Hit a Wall

It usually starts the same way.

You have a clear business need — expansion, equipment, a commercial property purchase, a cash flow gap. You walk into your bank, the one you’ve had an account with for a decade, expecting a straightforward conversation. What you get instead is a document checklist longer than your business plan, a credit analyst who’s never set foot inside a business like yours, and a timeline measured in weeks rather than days.

Three weeks later — sometimes six — you get a rejection letter. No explanation. No alternatives. Just a no.

This is not a rare story. According to a 2026 study, 61% of Australian SMEs abandoned their bank loan applications entirely due to documentation hurdles alone. Not because their businesses weren’t creditworthy. Not because the numbers didn’t stack up. But because the process broke them first.

This is exactly why the broker vs bank commercial loan debate has become one of the most important conversations in Australian business finance today — and why the answer, for a growing majority of business owners, is increasingly clear.

What Is a Broker vs Bank Commercial Loan, Really?

Before we go deeper, let’s clarify what we’re actually comparing.

When you approach a bank directly for a commercial loan, you are applying to a single lender, under their specific credit policies, through their internal systems, assessed by their in-house team. Their job is to protect the bank’s capital. Your job — making a living, growing a business — is secondary to that objective.

When you work with a commercial finance broker, you are working with a specialist who sits on your side of the table. A broker accesses multiple lenders simultaneously — major banks, non-bank lenders, private credit providers, specialist commercial lenders — and structures your application to match the right lender to your exact situation.

That structural difference is everything. In a broker vs bank commercial loan scenario, the bank asks: “Does this borrower fit our box?” The broker asks: “Which lender’s box fits this borrower best?”

Why Banks Reject So Many Commercial Loan Applications

The 61% abandonment stat doesn’t happen by accident. Banks are not designed to serve the complex, variable, asset-rich but cash-flow-irregular world of Australian SMEs. They are designed for predictability.

Here’s what banks look for — and where SMEs consistently fall short:

- Two or more years of clean, consistent financials

Banks want to see steady, upward-trending revenue. Seasonal businesses, businesses in growth mode, or those that have restructured recently are almost automatically flagged. A broker understands which lenders are comfortable with these profiles. - Standard industry categories

Banks lend easily to established sectors with clear collateral. Hospitality, creative industries, import-export businesses, professional services with irregular billing cycles — these often fall into “complex” territory that banks avoid. - Security that fits neatly on a balance sheet

Commercial property, equipment, or real estate as collateral is straightforward. Intellectual property, client contracts, inventory, or receivables-heavy businesses are harder for banks to value and fund. - Volume of documentation

Bank applications often require two years of business and personal tax returns, BAS statements, profit-and-loss statements, business plans, asset and liability schedules, and supporting explanations for any anomalies. Missing a single document can stall a case for weeks.

When you’re running a business, every week of delay has a cost. The broker vs bank commercial loan question isn’t just about interest rates — it’s about the real, measurable cost of time.

The Broker Advantage: More Than Just Access to More Lenders

It’s tempting to reduce the broker vs bank commercial loan comparison to “brokers have more lenders.” That’s true, but it undersells what a great broker actually does.

1. Pre-Assessment and Credit Positioning

A skilled commercial broker assesses your application before it goes anywhere. They review your financials, identify potential red flags, and either address them upfront or match you to a lender whose credit criteria those factors won’t trigger. This is the difference between a clean approval and a rejection that damages your credit file.

Banks don’t do this. They take your application, run it through their system, and either approve or decline. A broker shapes the application to succeed before it’s submitted.

2. Structuring for the Right Product

The broker vs bank commercial loan comparison also extends to product fit. Commercial finance is not one-size-fits-all. There are term loans, line of credit facilities, equipment finance, SMSF lending, invoice finance, bridging loans, commercial property loans, and more. Banks tend to push borrowers toward their standard products. A broker finds the structure that actually fits your cashflow cycle, your repayment capacity, and your business goals.

3. Negotiating Power

Brokers bring deal volume to lenders. That gives them negotiating leverage — on rates, on fees, on loan terms, on flexibility clauses — that an individual borrower approaching a bank directly simply doesn’t have. In a broker vs bank commercial loan context, the broker’s relationship with lenders often translates directly into better deal economics for you.

4. Speed of Approval

Banks can take four to eight weeks to assess and approve a commercial loan application. Non-bank lenders working with brokers often move in days. For a business with a time-sensitive opportunity — a commercial property acquisition, a supplier deal, a growth window — that difference is not a convenience. It’s a competitive advantage.

Broker Fees vs Bank Fees: Let’s Talk About the Numbers

One of the most common objections to using a broker is cost. “Won’t I pay more in broker fees?” The answer, when you look at the full picture, is almost always no — and often the opposite is true.

Bank fees you may not realise you’re paying:

- Application fees (typically $500–$2,000+)

- Valuation fees ($500–$1,500 for commercial property)

- Legal fees for security documentation

- Account management fees

- Early repayment penalties

- Annual review fees on some facilities

How brokers are typically paid:

Most commercial brokers are paid a commission (upfront and/or trail) by the lender — not by you. This commission is disclosed to you as part of the credit assistance process under Australian law. In some specialist or complex transactions, a broker may charge a brokerage fee, but this is disclosed upfront and is typically offset by the better rate or product they secure.

When you factor in the time saved, the cost of a rejected application on your credit file, and the rate differential a broker can negotiate, the broker vs bank commercial loan comparison consistently favours the broker on total cost — not just on sticker rate.

Broker Approval Rate vs Bank Approval Rate: The Real Comparison

Banks approve commercial loans at a lower rate than brokers — and the gap has been widening.

The major Australian banks have tightened commercial lending criteria significantly over the past three years, particularly for SMEs, following APRA guidance and their own internal risk recalibrations. Meanwhile, the non-bank lending market in Australia has grown substantially, with a broader range of products and more flexible credit policies.

Brokers with strong lender panels — including non-bank lenders, private credit providers, and specialist commercial lenders — achieve approval rates significantly above what SMEs can achieve approaching banks directly. This is partly because of product breadth, partly because of pre-assessment and positioning, and partly because of lender relationships.

In the broker vs bank commercial loan discussion, this approval rate differential is perhaps the most important data point of all. A loan that doesn’t get approved doesn’t just delay your plans — it costs you the opportunity itself.

Mortgage Broker vs Bank Australia: Why the Market Has Shifted

The broker channel now writes more than 70% of residential mortgages in Australia. The commercial finance market is following the same trajectory, for the same reasons.

Australian business owners have become more financially literate. They understand that their bank, for all the history of the relationship, is not their advocate. A bank’s job is to lend money at a profit. A broker’s job is to find the best loan for your situation. These are fundamentally different mandates.

The ASIC and MFAA regulatory frameworks that govern commercial brokers in Australia also mean that brokers are legally required to act in your best interest — they must recommend a product that is not unsuitable for your situation and must disclose any conflicts of interest, including commissions. This accountability framework is part of why the broker vs bank commercial loan choice is increasingly straightforward.

Why Use a Broker for a Business Loan? The Situations Where It Matters Most

Let’s get specific. The broker vs bank commercial loan equation is especially clear in these situations:

You are self-employed or have variable income

Banks want clean, consistent PAYG-style income documentation. Self-employed borrowers, business owners, and sole traders with variable income often don’t fit this mould. Brokers have access to lenders with low-doc and alt-doc products specifically designed for these borrowers.

You need a commercial property loan

Commercial property finance is more complex than residential. LVRs, lease terms, property use, tenant quality, and zoning all affect lender appetite. A broker who specialises in commercial property finance knows which lenders are active in which asset classes and can structure a deal that a bank might decline.

You have an unusual business structure

Trusts, SMSFs, complex company structures, or businesses with related-party transactions can trigger bank compliance concerns. Experienced commercial brokers deal with these structures routinely and know which lenders are comfortable with them Broker vs bank commercial loan.

You need funds quickly

If you have a 30-day settlement on a commercial property, or a supplier deal that expires in two weeks, a bank’s eight-week approval timeline simply doesn’t work. A broker with access to fast-approval non-bank lenders can often get you unconditional approval in 48–72 hours for the right deal.

You’ve been declined before

A bank decline is not the end of the road. It is, in fact, often the beginning of the broker conversation. A good broker will understand why you were declined, address those factors, and match you to a lender whose criteria you do meet.

What to Look For in a Commercial Finance Broker

Not all brokers are equal. In the broker vs bank commercial loan decision, the quality of the broker matters as much as the channel itself.

Lender panel breadth

How many lenders does the broker have accreditation with? A broker with 10 lenders on panel has fundamentally different capability than one with 40+. In commercial finance, you want a broker with access to major banks, second-tier banks, non-bank lenders, and specialist commercial lenders.

Commercial finance specialisation

Commercial lending is a different discipline from residential mortgage broking. Look for a broker who specialises in business and commercial finance — who understands cash flow lending, equipment finance, commercial property, and working capital structures.

Transparency and disclosure

A trustworthy broker discloses their commissions, explains why they’re recommending a particular product, and doesn’t rush you into a decision. If a broker can’t clearly explain the fee structure or why one lender is better for you than another, that’s a warning sign.

Track record with businesses like yours

Ask for examples. A broker who has successfully placed loans for businesses in your sector, of your size, with your financial profile, is far more valuable than one with general experience.

The Real Cost of Choosing the Bank Without Exploring Your Options

Let’s be honest about what’s at stake in the broker vs bank commercial loan decision.

If you apply to a bank and get declined, you have:

- Lost four to eight weeks of processing time

- Taken a hard credit enquiry on your credit file

- Missed the opportunity (if it was time-sensitive)

- Started from zero, having to approach the market again

If you work with a broker from the start:

- You submit one application that goes to the most suitable lender(s)

- You get professional pre-assessment before any credit is checked

- You are matched to a lender with the highest probability of approval

- You receive ongoing support through the settlement process

The broker vs bank commercial loan calculation, when you map the full risk and cost, consistently favours starting with the broker.

Efficient Capital: Sydney’s Commercial Finance Specialists

This is where Efficient Capital Solutions comes in.

Based in Greater Sydney, Efficient Capital is a full-service finance brokerage with a specialist commercial lending capability. Their team — led by directors Rohit Lakhotia and Joshua Martin, with a highly experienced team of credit analysts and finance consultants — understands the difference between a loan that gets approved and a loan that gets declined Broker vs bank commercial loan.

Efficient Capital’s lender panel spans major banks, non-bank lenders, private credit providers, and specialist commercial lenders. They work across:

- Commercial property loans — including owner-occupied and investment commercial property

- Business loans — term facilities, lines of credit, and working capital solutions

- Equipment finance — for asset acquisition across all sectors

- SMSF lending — for trustees looking to acquire property through their fund

- Invoice finance and trade finance — for cash flow and working capital needs

- Bridging loans — for time-sensitive acquisitions and transitions

- Private lending — for complex, non-standard situations

When it comes to the broker vs bank commercial loan question, Efficient Capital’s answer is built into how they work: they assess your situation first, identify the right structure, match you to the right lender, and manage the process through to settlement.

If you’re a business owner in Greater Sydney — or anywhere in Australia — who has been declined by a bank, is worried about documentation requirements, or simply wants to know whether there’s a better option than your current bank, the conversation starts with Efficient Capital.

Frequently Asked Questions

Is a broker vs bank commercial loan more expensive?

Not typically. Brokers are usually paid by the lender, not by you. And their ability to negotiate rates, structure products correctly, and access non-bank lenders often results in a better overall cost than a direct bank application.

Does using a broker affect my credit score?

A good broker does thorough pre-assessment before submitting any formal application, minimising unnecessary credit enquiries. This is a significant advantage over applying to multiple banks directly.

How long does it take to get a commercial loan through a broker?

It depends on the lender and the complexity of the deal. Non-bank lenders working through brokers can approve and settle in days for the right transaction. More complex commercial property deals may take two to four weeks — still typically faster than a bank. Broker vs bank commercial loan

What documents do I need to provide a broker?

Less than you’d expect. A broker will typically ask for recent BAS statements, business and personal tax returns, a summary of your borrowing needs, and an overview of your business. They take it from there.

Can a broker help if I’ve been declined by a bank?

Yes — this is one of the most common starting points for broker conversations. A bank decline doesn’t mean you can’t borrow. It means you need a different lender or a different structure.

The Bottom Line on Broker vs Bank Commercial Loan

The data is clear. The 2026 study showing 61% of SMEs abandoning bank applications is not a anomaly — it’s a signal. Banks are not structurally equipped to serve the complexity, diversity, and urgency of Australian business finance needs.

The broker vs bank commercial loan decision is, in most cases, not a close call. Brokers offer broader access, better positioning, faster approval, competitive rates, and genuine advocacy. Banks offer a single product, a single credit policy, and a process designed primarily to serve their own risk management requirements.

If your business needs commercial finance — whether for property, equipment, growth, cash flow, or any other purpose — the smartest first call is not to your bank. It’s to a commercial finance specialist who works for you.

Ready to Find the Right Commercial Loan for Your Business?

Stop wasting time on bank applications that lead nowhere.

The team at Efficient Capital Solutions has helped hundreds of Australian businesses find the right commercial finance — faster, with better terms, and without the documentation nightmare of going direct to a bank.

Get in touch with Efficient Capital today — and find out what your business actually qualifies for.

Or explore their commercial finance services directly: Commercial Finance — Efficient Capital

Efficient Capital Solutions is a full-service finance brokerage based in Greater Sydney, Australia. Their team of experienced finance consultants and brokers specialises in commercial loans, business loans, home loans, and working capital finance Broker vs bank commercial loan.