Help to Buy Scheme Australia 2026: The Complete Shared Equity Guide

For many buyers in Sydney, the challenge is no longer about wanting to own a home. It is about figuring out how to enter the market without overextending financially. Over the past few years, that question has shifted from “How fast can I save a 20% deposit?” to “Is there a smarter way to structure my entry?”

This is where government-backed pathways like the Help to Buy Scheme Australia come into focus. Not as shortcuts, but as alternative entry strategies that change how ownership is structured from day one.

Why More Buyers in Sydney Are Exploring Alternative Paths to Homeownership

Property prices across Greater Sydney have made traditional entry increasingly difficult, even for dual-income households. Many buyers today are financially stable but deposit-constrained, which creates a gap between borrowing capacity and actual entry.

This is why interest in a government home buying scheme in Australia has grown. Instead of waiting years to accumulate a larger deposit, buyers are exploring models that allow them to enter earlier with structured support.

What Is the Help to Buy Scheme Australia, and How Does It Work?

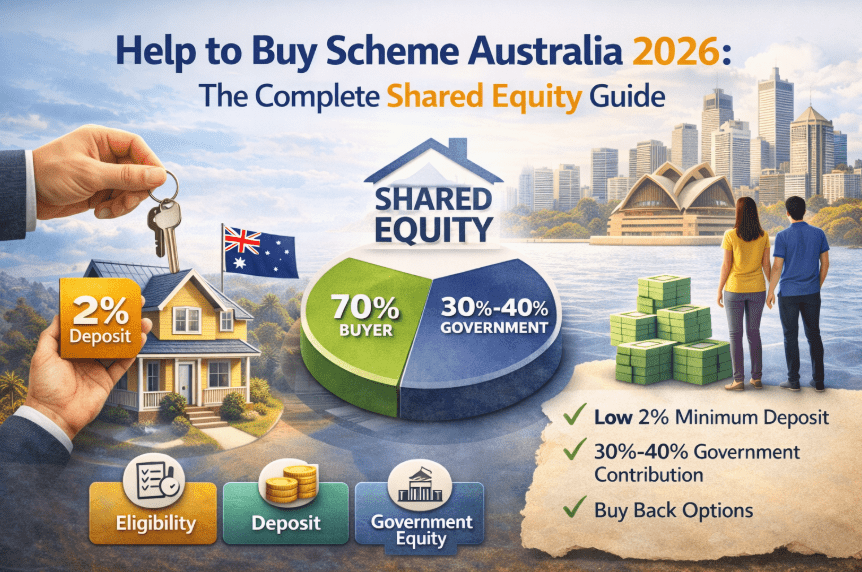

At its core, the Help to Buy Scheme Australia is a shared equity scheme home loan model. Instead of taking on the full cost of a property, the government contributes a portion of the purchase price. This reduces the amount you need to borrow and lowers your upfront requirements. In practical terms:

- Buyers can “save a minimum 2% deposit”

- The government may “contribute up to 30% for existing homes or 40% for new homes”

- The scheme is limited to “10,000 places each year”

This means you enter the market with a smaller loan, lower repayments, and no need to stretch your finances early on.

Key Features of the Help to Buy Scheme Australia 2026

The Help to Buy Scheme Australia 2026 is structured to address entry barriers while maintaining long-term flexibility. Key features include:

- Access to a 2% deposit home loan in Australia pathway

- Reduced loan size due to government contribution

- No requirement to pay LMI

- Gradual buyback of government equity over time

The broader rollout is expected to support around 40,000 Australian households, making it a significant national initiative rather than a niche offering.

Help to Buy Eligibility NSW (New South Wales): Who Can Apply?

Eligibility under the Help to Buy eligibility criteria in New South Wales is designed to prioritise genuine owner-occupiers, particularly those looking to enter the market for the first time in New South Wales (NSW). Typical requirements include:

- First home buyer status

- Income thresholds (single and joint applicants)

- Australian citizenship or permanent residency

- Intention to live in the property

An important detail is that property eligibility depends on location. As outlined in official guidelines, each participating state and territory has its own property price caps. This means what qualifies in NSW, especially in Sydney, is shaped by regional thresholds.

Understanding Property Price Limits in New South Wales (NSW)

For buyers in Sydney, price caps are not just a technical detail. They directly influence what type of property you can realistically consider under the scheme. For example, current guidance indicates that properties can be purchased up to $1.3 million in Sydney and regional centres, and up to $800,000 in the rest of the state.

This creates a structured boundary within which buyers need to plan their purchase. Rather than restricting choice, it encourages alignment between budget, eligibility, and long-term affordability.

What Shared Equity Actually Means for You as a Homeowner

The term shared equity scheme home loan can feel abstract at first, but the concept is straightforward.

- The government owns a percentage of your property

- You retain full rights to live in it

- You can gradually buy back that share over time

- When you sell, the government receives its proportional share

This structure reduces your initial financial burden, but it also means future gains are shared. Understanding this balance is key. It is not just about entering the market. It is about how ownership evolves over time.

Where This Scheme Fits in Your Financial Strategy

The Help to Buy Scheme Australia is not just a product. It is a financial positioning decision. It shifts the equation,

From: Large deposit + full ownership

To: Smaller deposit + shared ownership

For some buyers, this creates immediate access without compromising stability. For others, it introduces trade-offs around long-term equity. The key is not whether the scheme is available. It is whether it aligns with your income trajectory, your property goals, and your long-term financial plan.

Comparing Options: Help to Buy vs Traditional Home Loans

To make an informed decision, it helps to look at both paths side by side. Rather than focusing only on entry requirements, the real difference lies in how ownership, cost, and flexibility play out over time.

| Factor | Help to Buy Scheme | Traditional Home Loan |

| Deposit Requirement | As low as a 2 per cent deposit | Typically, 5% to 20%, depending on the lender |

| LMI (Lenders Mortgage Insurance) | Not required to pay LMI | Required if the deposit is below 20% |

| Loan Size | Lower (government contributes equity) | Higher (buyer funds full property) |

| Ownership Structure | Shared with the government | Full ownership from day one |

| Monthly Repayments | Generally lower | Higher due to a larger loan |

| Capital Gains | Shared proportionally | Fully retained by owner |

| Flexibility | Structured, with buyback options | Full control over property and equity |

This creates a clear trade-off: lower upfront cost and easier entry versus full ownership and long-term equity control. Neither approach is universally better. The right choice depends on how you prioritise access, flexibility, and long-term financial outcomes.

When the Help to Buy Scheme Australia Makes Sense

The scheme tends to work well when:

- You have a stable income but limited savings

- You want to enter the market sooner rather than later

- You plan to live in the property long-term

- You prioritise manageable repayments over full ownership upfront

In these scenarios, shared equity can act as a bridge into ownership, not a compromise.

When You May Want to Explore Other Financing Structures

There are also situations where a different approach may be more suitable:

- You prefer full ownership from the beginning

- You are targeting high-growth investment areas

- You expect to reach a higher deposit threshold soon

- You want complete control over future capital gains

This is where structuring becomes important. The scheme is one option, not the only one.

Structuring Your Home Purchase Beyond Just the Scheme

Buying a home is not just about eligibility. It is about how the entire financial structure is built around it. Factors such as offset accounts, redraw facilities, fixed vs variable repayments, and family guarantee options can significantly influence your outcome over time.

This is where working with a team experienced in Efficient Capital’s personal finance solutions can help bring clarity to the process. Their approach focuses on aligning loan structure with long-term financial efficiency, rather than just securing approval.

Looking at the Bigger Picture: Grants, Schemes, and Combined Strategies

The Help to Buy Scheme Australia does not exist in isolation. Many buyers benefit from combining:

- Government grants

- Stamp duty concessions

- Structured loan products

Understanding how these elements work together can create a more balanced and sustainable entry strategy. For a broader view of available pathways, resources like Efficient Capital’s guide on first home buyer grants provide useful context on how different schemes can complement each other.

How Financial Advisory Helps You Make the Right Call

At a glance, the scheme seems straightforward. But the real decision lies in understanding what you gain today and what you may give up tomorrow. A structured advisory approach helps evaluate repayment sustainability, equity implications, and alternative financing pathways. Rather than focusing on eligibility alone, it shifts the conversation to outcomes.

A Clearer Way to Approach the Help to Buy Scheme in Australia

The Help to Buy Scheme Australia is neither a shortcut nor a compromise. It is a different way of entering the property market. For some, it is a practical step toward ownership sooner. For others, alternative structures may offer greater long-term efficiency. What matters is not just whether you use the scheme, but whether your decision is backed by clarity, context, and a well-structured financial plan.

If you’re considering your options, speaking with a team like Efficient Capital can help you structure the decision with clarity.