Family Home Guarantee: How Single Parents Can Buy With Just a 2% Deposit

For many single parents in Australia, the decision to buy a home rarely begins with browsing listings. It starts much earlier, often with a quiet assumption that the numbers simply will not work. The most common version of that assumption is familiar: you need a 20% deposit to buy a home. Without it, the door to ownership stays closed.

In the single-parent home loan Australia context, that belief carries even more weight. Saving tens of thousands while managing a household on one income is not just difficult. For many, it feels unrealistic enough to stop the process before it begins. That is where the conversation around the family home guarantee needs to shift. Not because the system has become easier, but because it has changed in ways that are often overlooked.

Why That Assumption Is No Longer Fully True

The 20% deposit rule still exists in Australia, but it is no longer the only path into the property market.

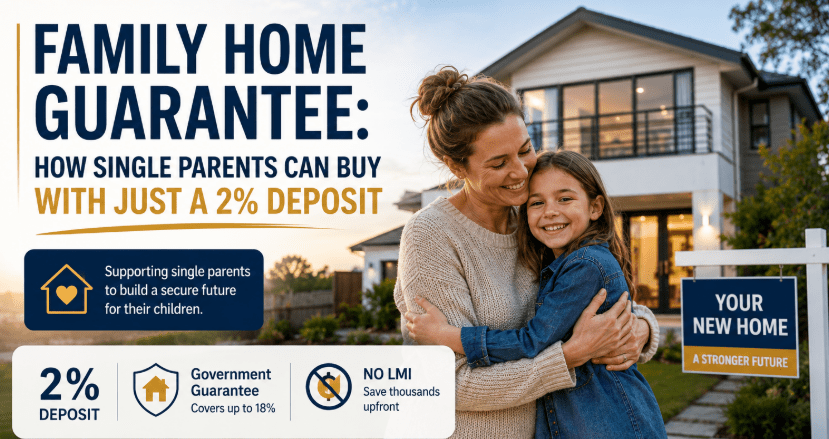

The family home guarantee scheme was introduced to support single parents and single legal guardians who might otherwise be locked out of home ownership due to deposit requirements. Under this scheme, eligible applicants can purchase a home with as little as a 2% deposit, with the government guaranteeing the remaining portion that would typically be required by lenders.

This is not a minor adjustment. It is a structural shift in how entry into the housing market can work for a specific group of buyers. According to the official Housing Australia – Family Home Guarantee page, eligible single parents or guardians can buy a home with a deposit as low as 2%.

What You’re Really Putting Down with a 2% Deposit

At first glance, the idea of a 2% deposit can feel almost too good to be true. In practice, it is more precise than it sounds.

If a property is valued at $600,000, a 2% deposit comes to $12,000. Under traditional lending conditions, a buyer would typically need around $120,000 to avoid additional costs like Lenders Mortgage Insurance (LMI). The gap between those two numbers is significant.

Through the Housing Australia Family Home Guarantee, the government guarantees up to 18% of the property value. This effectively removes the need for LMI and allows lenders to proceed with a much smaller upfront contribution from the borrower.

However, this is where clarity matters. The scheme does not make loans easier to qualify for. Banks still assess income, expenses, credit history, and overall serviceability. The difference is that the deposit barrier is reduced, not the lending standards.

The official factsheet also confirms that the scheme is designed for eligible single parents or legal guardians with at least one dependent child, and that approximately 5,000 guarantees were made available each financial year up to June 2025.

The Bigger Challenge Is How the Scheme Actually Works in Practice

This is where the conversation often shifts from possibility to complexity. Most people assume that once the deposit requirement is lowered, the process becomes straightforward. In reality, the deposit is only one part of the equation. What tends to create friction is everything around it:

- Not all lenders participate in the scheme

- Each lender may interpret eligibility and risk slightly differently

- Borrowing capacity still depends on income and financial commitments

- The way a loan is structured can influence whether it is approved

Two applicants with the same deposit and similar incomes can have very different outcomes depending on how their application is presented and which lender they approach. This is the part of the process that is less visible but often more decisive than the deposit itself.

Where Location Changes Everything: Sydney and Victoria

While the scheme is national, its impact is shaped by where you are buying. Property price caps apply under the scheme, and these caps vary depending on location. In higher-cost markets like Greater Sydney, the caps are higher, but so is competition and overall property pricing. In Victoria, the difference between metropolitan and regional areas can influence both affordability and eligibility.

This creates a practical reality. The scheme opens the door, but it does not standardise what sits behind it. A property that fits comfortably within the cap in a regional area may be harder to find within the same limits in a capital city. For a single parent first home buyer, this often means balancing three factors at once:

- Budget and borrowing capacity

- Property availability within price caps

- Long-term lifestyle and location needs

Understanding how these interact can make a significant difference to how viable the scheme feels in practice. For those exploring broader support options alongside the scheme, it can also be helpful to understand what other grants may apply.

Family Home Guarantee Eligibility: Who This Actually Works For

Eligibility under the scheme is relatively clear on paper, but it is worth understanding what it looks like in practice. To qualify, applicants generally need to:

- Be a single parent or single legal guardian

- Have at least one dependent child

- Intend to live in the property as an owner-occupier

- Meet income and borrowing requirements set by lenders

The family home guarantee eligibility criteria are designed to be accessible, but they are not automatic. Income stability, existing financial commitments, and overall borrowing capacity still play a central role in whether a loan is approved.

The Treasury’s housing policy overview reinforces that the Single Parent stream supports eligible applicants with deposits as low as 2%, but within a broader framework of responsible lending. In other words, eligibility opens the opportunity. It does not guarantee the outcome.

Why Many Eligible Buyers Still Don’t Move Forward

One of the more interesting patterns with the scheme is that a number of eligible buyers still hesitate or stall in the process. This is rarely because the opportunity is not there. It is usually because the path forward is unclear. Common challenges include:

- Not knowing which lenders actually offer the scheme

- Misjudging borrowing capacity and affordability

- Missing opportunities to combine the scheme with other forms of support

- Uncertainty about how to structure the loan correctly

These are not headline issues, but they are often the reasons applications do not progress. It is also where the difference between understanding a scheme and using it effectively becomes more visible.

Turning the Family Home Guarantee Into a Real Home Loan

At this stage, the focus shifts from what the scheme offers to how it is applied. This is where practical guidance can make a difference. Matching an applicant with a lender that participates in the scheme, structuring the loan in a way that aligns with lending criteria, and integrating available grants or concessions all contribute to whether an application moves forward smoothly.

For buyers in competitive markets, particularly in Sydney, comparing and selecting the right loan option becomes even more important. The goal is not simply to access the scheme, but to translate it into a workable and sustainable home loan.

What This Tells Us About Where the Market Is Headed

If you step back for a moment, this isn’t just about one scheme. Over the past few years, there’s been a noticeable shift in how the government is trying to help people get into the housing market. It’s less about asking buyers to meet a fixed deposit target, and more about finding ways to reduce that upfront hurdle without loosening lending standards too much.

That’s where schemes like this come in. In fact, government figures show that more than 240,000 first home buyers have already been supported through deposit-style schemes. That gives you a sense of the direction things are moving in.

The Family Home Guarantee sits within that broader shift. It’s not a one-off opportunity or a workaround. It’s part of a wider effort to make home ownership more achievable for people who would otherwise spend years trying to catch up on a deposit.

So What Really Changes for You as a Buyer

It’s easy to look at the 2% figure and think this is simply about needing less money upfront. But in practice, it changes something slightly different. Instead of spending years trying to reach a 20% deposit, some buyers can start the process earlier than they expected. That doesn’t mean skipping steps. It just means those steps begin sooner.

You still need to qualify. Your income still needs to hold up. The property still needs to fit within the rules. None of that disappears. What shifts is the starting point. For a lot of single parents, that can make a real difference. The focus moves away from “how long will it take me to save enough?” to “am I in a position to move forward now, if everything lines up?”

And that’s usually where things become more practical. Understanding how the scheme works is one part of it. The other part is figuring out how it fits your situation, your borrowing capacity, and the kind of property you’re actually looking at. That’s the point where the idea turns into a decision.